Submission to the House of Commons Standing Committee on Finance

Recommendations

The Government of Canada should:

- Reconsider the FI tax and CRD and recommit to the principle of tax neutrality. At a minimum, the Government needs to commit to a firm sunset date for the FI tax to give investors and those working in the banking sector confidence that Canada is committed to attracting investment.

- Only proceed to implement Pillar 2 of the OECD Inclusive Framework when it is clear that Canada’s primary competitors are taking action to do so and should only proceed at the same pace as those jurisdictions.

- Undertake a comprehensive review of Canada’s tax system to better align it to the needs of Canada’s evolving economy and to ensure Canada can encourage growth and investment to compete internationally.

- Collaborate with industry to develop measures like targeted investments or tax incentives, while taking a balanced and flexible approach to any new regulatory obligations, to meet Canada’s net zero emission targets while increasing productivity and economic growth.

- Extend the Accelerated Investment Incentive and review its eligibility criteria.

- Create a consumer protection and redress framework for non-bank payment services providers, building on the Retail Payments Activities Act.

- Review the AML/ATF framework to ensure it is risk-based, priority-focused, collaborative, and innovative, and should establish a single pan-Canadian federal beneficial ownership registry encompassing both federally and provincially regulated corporations.

- Develop a holistic approach to cryptocurrency regulation that is principles-based and technology- neutral.

- Develop policy centred on the objective of creating a seamless national market for the movement of capital, goods and services, workers and energy.

Introduction – Banking Powers Canada’s Economy

Canada’s banks play a pivotal role in the economy.

- The banking industry accounts for 3.8% of Canadian GDP, up from 2.9% 10 years ago.

- Banks are among the largest Canadian taxpayers, with the six largest banks paying $12.5 billion in tax to all levels of government in Canada in 2020.

- Canadian banks provided $21.3 billion in dividend income in 2020 and a further $22.6 billion in 2021 – dividends that went to seniors, families, pension plans, charities and endowments.

- The banking industry employs more than 280,000 people, making it a leading source of full-time, well-paying jobs across the country. Banking industry employment has grown by 8.3% over the last 10 years.

- Banks authorized $1.52 trillion in credit to Canadian businesses as of 2021. Of that, $269.1 billion went to 1.72 million small-and-mid-sized businesses.

- With a network of over 5,780 branches, Canadian banks are the anchor of communities nationwide.

- The banking industry invests heavily in new technology to meet the needs of Canadians. In the last decade, Canadian banks have invested nearly $100 billion in technology.

Banks recognize the important role they play in Canada’s economy and have proven time and again that they work with Canadians during challenging times. During the COVID crisis, banks stepped forward to provide relief to individuals and businesses providing:

- more than 800,000 mortgage payment deferrals,

- more than 1,290,000 payment deferrals for credit cards, credit lines, personal loans, and auto loans,

- waiving a total of $117,000,000 in fees.

In addition, banks and other financial institutions partnered with the federal government to provide CEBA loans to nearly 900,000 small businesses, and banks extended an additional $ 49.2 billion in credit to business customers.

FI Tax and CRD

An efficient tax system is one that is neutral. A neutral tax system incorporates relatively low and relatively flat rates, with a broad base and with equal and proportionate application. This lets markets work to direct investment to its best use. A neutral tax system encourages growth and innovation by letting investors, savers and employees make choices driven by where they can get the best return for their capital, labour or knowledge, rather than by tax considerations. The Financial Institutions (FI) Tax and Canada Recovery Dividend (CRD) are inconsistent with the principle of tax neutrality. Internationally, the imposition of the FI Tax and CRD is being noticed by investors, and is causing them to question Canada’s commitment to building an economic environment that promotes investment. Domestically, the FI Tax and CRD will have an impact on the millions of retail Canadian investors who hold bank shares and the 280,000 Canadians working in the sector. The Government needs to reconsider the FI Tax and the CRD and to recommit to the principle of tax neutrality. At a minimum, the Government needs to commit to a firm sunset date for the FI Tax to give investors and those working in the banking sector confidence that Canada is committed to attracting investment.

International Corporate Tax Reform

In Budget 2022, the government stated its intention to implement "Pillar 2" of the OECD’s international tax reform plan, which calls for, among other measures, a minimum corporate tax rate among participating jurisdictions and a coordinated system of jurisdictional taxation rights. To be effective, Pillar 2 requires widespread adoption. While several countries have made verbal commitments to implement Pillar 2, to date it has not been adopted by the principal jurisdictions. To avoid putting Canada at a competitive disadvantage and discouraging investment, the Government should only proceed with Pillar 2 when it is clear that substantially all other major jurisdictions, including the U.S., have taken material steps to implement it.

Focus on Productivity

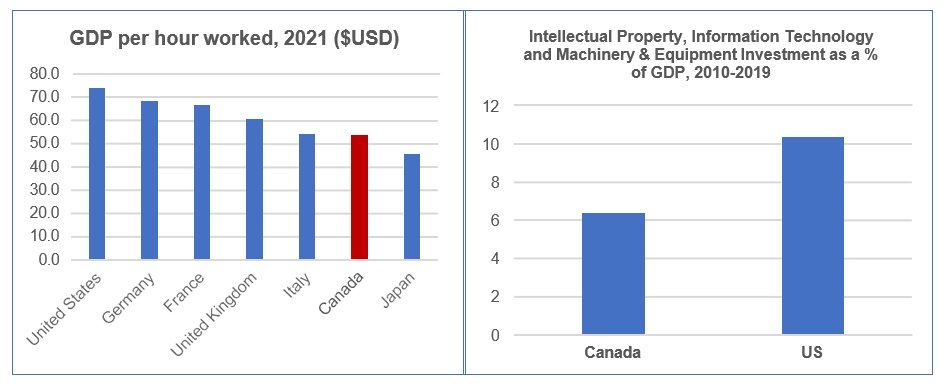

Canada has a productivity challenge.

- Canadian labour productivity is among the lowest in the G-7.

- Investment in productivity-enhancing areas of intellectual property, information technology and machinery & equipment is happening at half the rate in Canada compared to the U.S.

OECD (2022), GDP per hour worked (indicator). doi: 10.1787/1439e590-en (Accessed on 26 September 2022)

OECD (2021), OECD Compendium of Productivity Indicators, OECD Publishing, Paris, https://doi.org/10.1787/f25cdb25- en (accessed on 26 September 2022).

Canada needs a taxation system that promotes investment, encourages growth, and improves productivity. While the solution to Canada’s productivity challenge is not found solely in taxation, taxation plays an important role in building an economic climate that encourages growth and productivity. The Government of Canada should undertake a comprehensive review of Canada’s tax system to align it to the needs of Canada’s evolving economy and to ensure Canada can compete internationally. A comprehensive review should encompass income tax, commodity tax and other forms of taxation. A review would also afford an opportunity to assess measures that could encourage the investments that will be needed to transition to net zero. A study by RBC indicated that Canada will need an estimated $2 trillion over the next 30 years to finance the transition.1 In the near term, to encourage investment, the Government should extend the Accelerated Investment Incentive and review eligibility criteria to support broader investment opportunities.

Enabling the Transition to Net Zero

Transitioning to net zero presents challenges and opportunities. A collaborative process will be needed to allow Canada to meet our climate goals while enhancing productivity and growth. The Government should collaborate with industry to design targeted investments and tax incentives while taking a balanced and flexible approach to any new regulatory obligations. The banking sector is committed to doing its part. Banks are active individually and in collaboration with governments, clients, and stakeholders, to explore options that promote sustainable finance and work towards net zero. Canadian banks are also key participants in the federal government’s Sustainable Finance Action Council.

Future-Proofing Finance

The financial sector has been at the forefront of innovation. How Canadians engage with their financial institution and transact has been transformed by technology.

- Electronic payments now represent 79% of transactions – accounting for 15.8 billion transactions in 2020.2

- Nearly two thirds (65%) of Canadians used mobile app-based banking last year, and more than a third of financial transactions are done with a mobile device.3

Technology has enabled an explosion of competition. There are estimated to be over 2000 non-bank payment services providers operating in Canada.4

Initiatives such as Payments Canada’s Payments Modernization Project and the federal government’s Open Banking initiative will accelerate these trends. The Government needs to recognize this context as it considers its next steps on the Retail Payments Oversight Framework, AML, and digital currencies.

Retail Payments Oversight

In response to the growth of unregulated payment services, the Government enacted the Retail Payments Activities Act, which empowers the Bank of Canada to supervise payment services providers. The CBA welcomed this development; however, at this stage the framework focuses on:

- registration;

- operational risk;

- safeguarding funds; and

- reporting

but excludes consumer protection. Payment services providers deal directly with consumers, so the absence of consumer protection is a significant shortcoming. The CBA recommends that the Government create a consumer protection and redress framework as part of its retail payments oversight framework.

Anti-Money Laundering

The banking industry recognizes its key role in combating money laundering and terrorist financing. Our focus is on strengthening the regime by

- emphasizing a risk-based and priorities-focused approach,

- improving collaboration,

- facilitating innovation,

- and improving transparency of beneficial ownership.

The CBA has advocated for a comprehensive, federally-maintained beneficial ownership registry, which would include information on both federally and provincially regulated corporations and other legal arrangements (including partnerships, trusts, and associations). We appreciate the government’s commitment to improve transparency by establishing a beneficial ownership registry for federal companies and properties. While that is valuable, it is essential that the solution is built as a single pan- Canadian federal registry, including beneficial ownership information on federally and provincially regulated corporations and other legal arrangements. Moreover, we need to ensure that legislation progresses to allow for resources and activity to be targeted at areas of the highest risk and facilitates collaboration and the lawful sharing of information between financial institutions, and from FINTRAC and law enforcement to financial institutions.

Digital Currencies

The acceleration of e-commerce has brought the issue of digital currencies to the forefront. The CBA believes that government agencies must collaborate as the government focuses on digitalization of money during the first phase of the financial sector legislative review. The CBA supports a holistic, risk- based approach to the cryptocurrency regulation, including stablecoins, that provides clarity and promotes confidence and stability in financial markets while also enabling innovation. The policy objectives on the potential issuance of a Canadian Central Bank Digital Currency (CBDC) must be clearly established and verified in light of the risks to the stability of the financial sector. The potential unintended impacts of a CBDC on Canada’s payments ecosystem must also be considered.

Canada Needs an Integrated National Market

Canada is a federation of diverse regions, each with its own economic strengths and this creates both challenges and opportunities. Diversity in all its dimensions – economic, cultural, linguistic – is a source of strength for Canada. But to capitalize on diversity, Canada needs to ensure that goods and services, workers, and capital can move freely within our borders to allow the internal market to direct resources to those businesses that show the greatest promise. While we have made some progress, frictions persist that make it challenging for goods, services, capital, workers, and more recently energy, to move between regions. Public policy should be centred on the objective of creating a seamless national market for the movement of capital, goods and services, workers and energy.

The Time is Now

Canada is emerging from a challenging period. Having weathered COVID-19, we must face the challenge of generating a sustained period of strong economic growth to pay the debts that were incurred to make it through that crisis. Moreover, we need to do so while transitioning to a net zero. To meet these demands, Canada needs an economic plan focused on growth and productivity that leverages the advantages of Canada’s diversity in all its forms.

1 RBC, The $2 Trillion Transition: Canada’s Road to Net Zero, October 2021.

2 Payments Canada’s Canadian Payment Methods and Trends Report 2021.

3 CBA How Canadians Bank. December 2021. (https://cba.ca/technology-and-banking)

4 "Bank of Canada’s Ron Morrow: Fintechs 'need to be ready' for upcoming retail payments regulations", Betakit. August 17, 2022. (https://betakit.com/bank-of-canadas-ron-morrow-fintechs-need-to-be-ready-for-upcoming-retail-payments-regulations/)